Since the dawn of the internet, the titans of this industry have fought to win the “starting point” – the place that users start their online experiences. In other words, the place where they begin “browsing”. The advent of the dial up era had America Online mailing a CD to every home in America, which passed the baton to Yahoo’s categorical listings, which was swallowed by Google’s indexing of the world’s information – winning the “starting point” was everything.

As the mobile revolution continues to explode across the world – the battle for the starting point has intensified. For a period of time, people believed it would be the hardware, then it became clear that the software mattered most. Then conversation shifted to a debate between operating systems (Android or iOS) and moved on to social properties and messaging apps where people were spending most of their time. Today – my belief is we’re hovering somewhere in between apps and operating systems. That being said, the interface layer will always be evolving.

The starting point, just like a rocket’s launchpad, is only important because of what comes after. The battle to win that coveted position, although often disguised as many other things, is really a battle to become the starting point of commerce.

Google’s philosophy includes a commitment to get users “off their page” as quickly as possible…to get that user to form a habit and come back to their starting point. The real (yet somewhat veiled) goal, in my opinion, is to get users to search and find the things they want to buy.

Of course, Google “does no evil” while aggregating the world’s information, but they pay their bills by sending purchases to Priceline, Expedia, Amazon, and the rest of the digital economy.

Facebook, on the other hand, has become a starting point through it’s monopolization of users’ time, attention, and data. Through this effort – it’s developed an advertising business that shatters records quarter after quarter.

Google and Facebook, this famed duopoly, represent 89% of new advertising spending in 2017. Their dominance is unrivaled…for now.

Change is urgently being demanded by market forces – shifts in consumer habits, intolerable rising costs to advertisers, and through a nearly universal dissatisfaction with the advertising models that have dominated (plagued) the US digital economy. All of which is being accelerated by mobile. Terrible experiences for users still persist in our online experiences, deliver low efficacy for advertisers, and fraud is rampant. The march away from the glut of advertising excess may be most symbolically seen in the explosion of ad blockers. Further evidence of the “need for a correction of this broken industry” is Oracle’s willingness to pay $850M for a company that polices ads (probably the best entrepreneurs I know ran this company, so no surprise).

As an entrepreneur, my job is to predict the future. When reflecting on what I’ve learned thus far in my journey – it’s become clear that two truths can guide us in making smarter decisions about our digital future:

Every day, retailers, advertisers, brands, and marketers get smarter. This means that every day – they will push the platforms, their partners, and the places they rely on for users to be more “performance driven”. More transactional.

Paying for views, bots (Russian or otherwise), or anything other than “dollars” will become less and less popular over time. It’s no secret that Amazon, the world’s most powerful company (imho), relies so heavily on its Associates Program (it’s home built partnership and affiliate platform). This channel is the highest performing form of paid acquisition that retailers have, and in fact, it’s rumored that the success of Amazon’s affiliate program led to the development of AWS due to large spikes in partner traffic.

Chinese flag overlooking The Bund, Shanghai, China (Photo: Rolf Bruderer/Getty Images)

When thinking about our digital future, look down and look east. Look down and admire your phone – this will serve as your portal to the digital world for the next decade and our dependence will only continue to grow. The explosive adoption of this form factor is continuing to outpace any technological trend in history.

Now, look east and recognize that what happens in China will happen here, in the West, eventually. The Chinese market skipped the PC driven digital revolution – and adopted the digital era via the smartphone. Some really smart investors have built strategies around this thesis and have quietly been reaping rewards due to their clairvoyance.

China has historically been categorized as a market full of knock-offs and copycats – but times have changed. Some of the world’s largest and most innovative companies have come out of China over the past decade. The entrepreneurial work ethic in China (as praised recently by arguably the world’s greatest investor Michael Moritz), the speed of innovation, and the ability to quickly scale and reach meaningful populations have caused Chinese companies to leapfrog the market cap of many of their US counterparts.

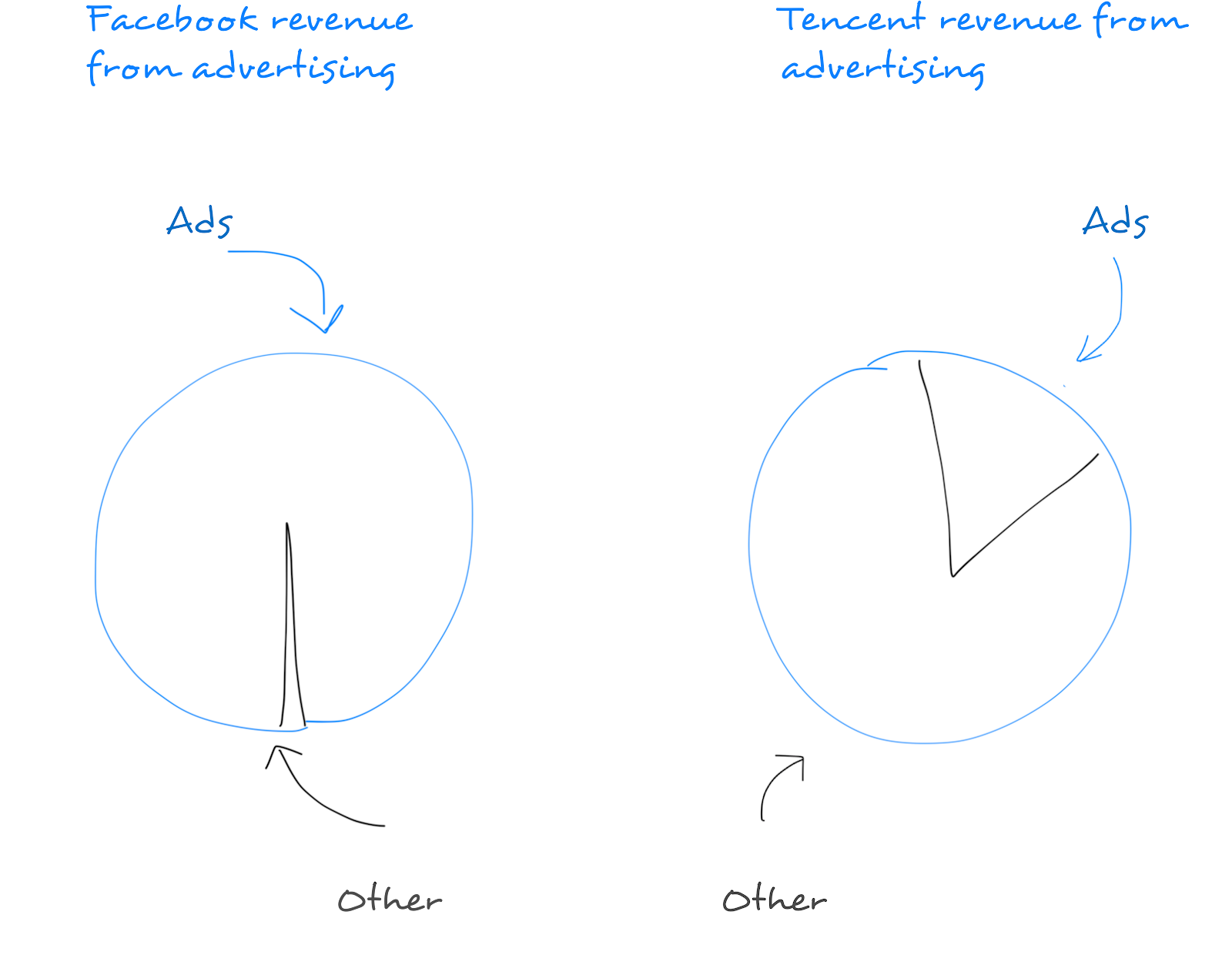

The most interesting component of the Chinese digital economy’s growth is that it is fundamentally more “pure” than the US market’s. I say this because the Chinese market is inherently “transactional”. As Andreessen Horowitz writes – WeChat, China’s most valuable company, has become the “starting point” and hub for all user actions. Their revenue diversity – is much more “Amazon” than “Google” or “Facebook” – it’s much more pure. They make money off the transactions driven from their platform – and advertising is far less important in their strategy.

The obsession with replicating WeChat took the tech industry by storm two years ago — and for some misplaced reason — everyone thought we needed to build messaging bots to compete.

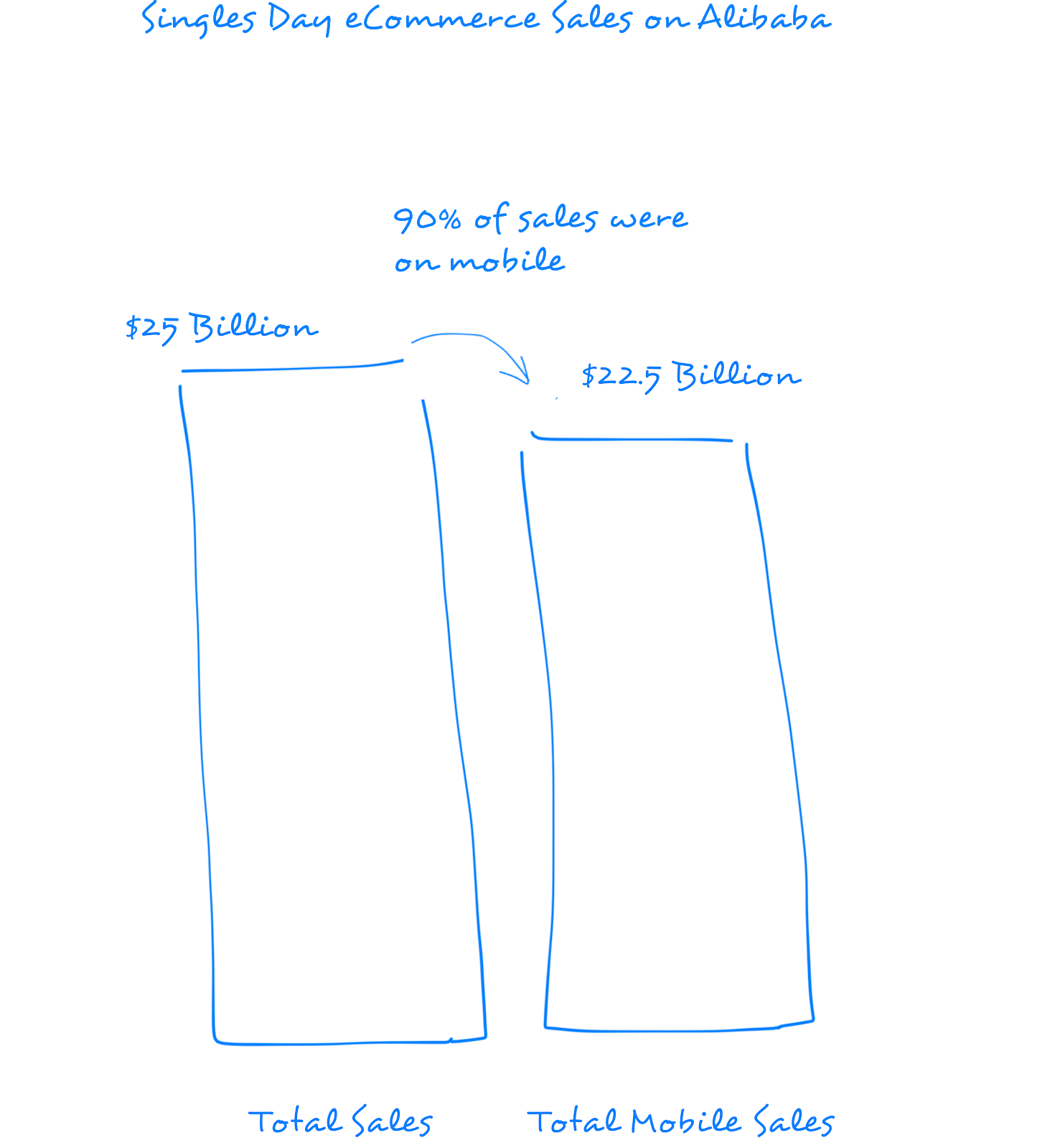

What shouldn’t be lost is our obsession with the purity and power of the business models being created in China. The fabric that binds the Chinese digital economy together and has fostered its seemingly boundless growth is the magic combination of commerce and mobile. Singles Day, the Chinese version of Black Friday, drove $25B in sales on Alibaba – 90% of which were on mobile.

The lesson we’ve learned thus far in both the US and in China are that “consumers spending money” creates the most durable consumer businesses. Google, putting aside all its moonshots and heroic mission statements, is a “starting point” powered by a shopping engine. If you disagree, look at where their revenue comes from…

Google’s announcement last week of Shopping Actions and their movement to a “pay per transaction model” signals a turning point that could forever change the landscape of the digital economy.

Google’s multi-front battle against Apple, Facebook, and Amazon is weighted. Amazon is the most threatening. It’s the most durable business of the 4 – and it’s model is unbounded on two fronts that almost everyone I know would bet their future on – 1) people buying more online, where Amazon makes a disproportionate amount of every dollar spent and 2) companies needing more cloud computing power (more servers), where Amazon makes a disproportionate amount of every dollar spent.

To add insult to injury, Amazon is threatening Google by becoming a starting point itself – 55% of product searches now originate at Amazon up from 30% just a year ago.

Google, recognizing consumer behavior was changing in mobile (less searching) and the inferiority of their model when compared to the durability and growth prospects of Amazon, needed to respond. Google needed a model that supported boundless growth and one that created a “win-win” for its advertising partners – one that resembled Amazon’s relationship with its merchants – not one that continued to increase costs to retailers while capitalizing on their monopolization of search traffic.

Google knows that with its position as the starting point – with Google.com, Google Apps, and Android – it has to become a part of the transaction to prevail in the long term. With users in mobile demanding less ads, and more utility (demanding experiences that look and feel a lot more like what has prevailed in China) – Google has every reason in the world to look down and to look east – to become a part of the transaction – to take its piece.

A collision course for Google and the retailers it relies upon for revenue was on the horizon. Search activity per user was declining in mobile and user acquisition costs were growing quarter over quarter. Businesses are repeatedly failing to compete with Amazon and unless Google could create an economically viable growth model for retailers – no one would stand a chance against the commerce juggernaut – not the retailers nor Google itself.

As I’ve believed for a long time, becoming a part of the transaction is the most favorable business model for all parties – sources of traffic make money when retailers sell things – and most importantly – this only happens when users find the things they want.

Shopping Actions is Google’s first ambitious step to satisfy all three parties – businesses and business models all over the world will feel this impact.

Good work, Sundar.

Read Full Article

No comments:

Post a Comment